The bitcoin mining hub has slowly been losing its dominance in the global hash market.

Over the past few weeks, Bitcoin markets have had to deal with a swarm of bad news coming out of China.

It started with rumors that miners in Sichuan had gone offline after the province limited energy-intensive industrial activities, such as Bitcoin mining.

Then came a joint statement by three of China’s top financial self-regulatory organizations reminding the public of the country’s 2017 ban on crypto assets. Then it was reported that for the first time, the Chinese State Council, headed by President Xi Jinping’s top economic advisor, was cracking down on mining.

To top things off, last Sunday the Chinese state-run news agency Xinhua published a negative article on crypto assets, denouncing their risks relative to traditional investment tools.

While there have been multiple factors contributing to this sell-off, one thing is undeniable: there is something brewing in China. Whatever it is, this series of events has led market participants to fear for Bitcoin’s future, especially as it relates to mining.

To get to the bottom of this, let’s follow the money.

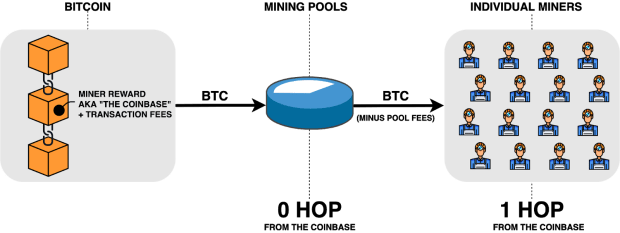

The great thing about Bitcoin’s financial transparency is that it enables us to evaluate how miners are responding to all of this, in realtime. But before we delve into the actual mining data, it’s important to do a quick recap of how miners interact with Bitcoin and how we can measure that.

One of the biggest misconceptions about Bitcoin mining is that it is, to quote Elon Musk, “highly centralized, with supermajority controlled by handful of big mining (aka hashing) companies.” This is objectively false. In reality, what we call mining nowadays is a highly layered activity.

In order to increase their odds of success, miners collectively contribute their resources to so-called mining pools. Pools represent large groups of individual miners that work together mining the very same block. When a pool successfully mines a block, it is awarded 6.25 newly issued BTC plus all fees paid by users to have their transactions included in that block. After collecting a service fee, the pool then distributes the proceeds to individual miners.

Tracking what happens to newly issued bitcoin can yield meaningful insights into the collective behavior of both mining pools and the individual miners operating within them. In order to discern these two very different actors, Coin Metrics has produced a set of aggregate metrics that serve as proxies.

As a proxy for mining pool behavior, we aggregate data from all “coinbase” transactions: the first transaction of every Bitcoin block (not to be confused with the exchange). As a proxy for individual miner behavior, we aggregate data one hop from that transaction, i.e., all transactions that received funds from the coinbase.

At a microscopic level, if you track what happens after one hop, the notion that Bitcoin mining is centralized is shattered. In fact, there are many transactions beyond one hop that have dozens of recipients, which may be indicative of layered structures even at the individual miner level. One theory is that several mining operations are joint ventures where partners may have complex payout structures. As such, measuring anything over one hop becomes more challenging and subjective.

Now that we have covered how aggregate miner behavior can be measured on-chain, let’s take a look at the data.

What is the on-chain data telling us? Before individual miners can effectively sell their coins, they must create a transaction that sends funds to an exchange, an over-the-counter desk, or even directly to the buyer albeit in rare circumstances. In any of these scenarios, we would see an increase in the flow of funds being sent from individual miners (one hop) to other addresses.

The chart below shows exactly that. Aggregate flows sent by miners are at the highest levels since March 2020, when markets crashed at the onset of the COVID-19 pandemic. This supports the hypothesis that the latest sell-off was by Chinese miners that have sold part of their holdings in order to escape the latest wave of enforcement actions by the Chinese Communist Party.

Although what they receive on a daily basis is small compared to global BTC volume, the data showcased above suggests that when miners are likely selling (an increase of “flows sent”), markets respond negatively.

Remember that miners are also speculators. Even though what they receive in miner rewards is small in USD terms relative to the volume of global BTC markets, they do hold BTC on their balance sheets. In times of uncertainty, when they expect to need cash, their collective actions affect the market.

Now put yourself in the shoes of a Chinese miner that might have to move to a different country. Regardless of the scale of your operations, you will likely need cash to finance that move. The good news is that this is a temporary phenomenon. As with previous spikes in flows sent, the market impact was short-term and close to coincidental.

Another interesting on-chain behavior worth highlighting is miners’ potential concerns towards centralized exchanges in light of the CCP’s crackdown. The current sell-off coincides with thousands of bitcoin being withdrawn from major exchanges and deposited to miner addresses, as shown below.

Interestingly, the CCP’s current crackdown on mining also coincides with a time of the year where some Chinese miners move their operations from Inner Mongolia to Sichuan. This 2,000km migration is motivated by the beginning of the rainy season in Sichuan, which increases the capacity of its hydroelectric power plants, thereby decreasing electricity costs.

It has been observed that the rainy season in China contributes to an increase in hash rate, a metric that indirectly tracks the resources being allocated to Bitcoin. However, if the CCP’s hawkish comments on mining in fact translate to enforcement actions, this seasonal migration might be impacted, and hash rate might see a drop from current levels.

If the CCP’s hawkish comments on mining in fact translate to enforcement actions that further motivate miners to emigrate from China, we might see a contraction in hash rate from current levels.

While it is still unclear how the Chinese mining community is tactically responding to this development, the market has reacted negatively in light of a potential decrease in hash rate. But if a decrease were to occur, how would this impact Bitcoin?

What if Hash Rate Crashes?

Another gigantic misconception about mining is that daily hash rate figures can provide an authoritative view of when miners are pulling the plug. This frequently generates panic, as people struggle with the notion that a large portion of miners have suddenly gone offline. Another Musk quote illustrates this misconception well when he claimed that when “A single coal mine in Xinjiang flooded, almost killing miners, […] Bitcoin hash rate dropped 35%.”

In reality, hash rate is not a precise metric. Hash rate formulas were designed to estimate how many computational resources are being allocated to a network on a given day. But there is a keyword that is often omitted in the metric’s name: implied. It’s called “implied hash rate” because it is impossible to get a precise daily change figure by solely looking at on-chain data.

If you look at the average daily Bitcoin implied hash rate on Coin Metrics’ dashboard (what people usually just call hash rate), you will see that large (35%+) fluctuations occur frequently.

Crypto media outlets often take advantage of hash rate fluctuations with sensationalist “BTC HASH RATE DROPS X%” headlines, but daily implied hash rate is, by its very design, a volatile metric that is not suitable to track lasting changes in the mining landscape.

The reason for this volatility is that all daily hash rate formulas are highly sensitive to how long blocks have been taking to be mined over a given lookup window. Since mining is an unpredictable process (a Poisson process to be precise), there is a probability that a Bitcoin block could take an hour to be mined without miners necessarily having gone offline (albeit a low-probability event).

In the example above, a probable event would push daily hash rate estimates down considerably, even in the event that no changes in the mining landscape have actually occurred. If you want to understand this more deeply, take a look at the formula we created at Coin Metrics to attempt to calculate daily implied hash rate figures, in the trillion of hashes per second (TH/s) unit.

As you can see above, all daily hash rate formulas, including Coin Metrics’, are highly sensitive to block times. Blocks that take longer to be mined decrease the block count in the 24-hour lookup window and push the implied hash rate downwards. Similarly, if blocks were found at a faster rate, which can also happen without new miners coming in, an increase in block count would push the implied hash rate upwards.

The only way to decrease the impact that these probable events have on hash rate estimates is to increase the measurement window. That is not to say that we need to abolish the 24-hour, 144-block, hash rate estimates. We just need to stop using it to make assertive claims about actual changes in hash rate when attempting to measure miner behavior.

If you want a more accurate representation of changes in Bitcoin’s hash rate, a much better metric is the one-month implied hash rate. As the name entails, this version of hash rate encompasses changes that might have taken place on a rolling 30-day window.

This metric looks much better on a time series because it filters out all of the noise that is naturally produced by large (but probable) changes in block creation time. As such, it is a much better suited metric to track mid to long-term changes in Bitcoin’s hash rate.

One-month implied hash rate is a better suited metric to track mid to long-term changes in Bitcoin’s hash rate because it filters out all of the noise that is naturally produced by large (but probable) variations in block creation time.

Just like the one-day hash rate metric, the one-month implied hash rate is also free to use. You don’t even have to sign up to check it out. Make sure to forward this to the next crypto journalist that uses one-day hash rate changes as click-bait.

So, what does all of this mean for Bitcoin?

Going through this hash rate exercise is important because we might be heading into a drastic shift in the composition and geographic location of Bitcoin miners if additional crackdowns by the CCP take place. And we will need accurate data to track the impact of a potential mass migration.

In doing research for this piece I reconnected with a fellow Bitcoiner based in China who thinks stronger enforcement action by the CCP is a matter of when, not if. This sentiment is shared by other industry analysts with much deeper expertise in deciphering the CCP’s actions.

It is no coincidence that The People’s Bank of China (PBOC) is scheduled to launch its own coin at some point this year. And Bitcoin is at complete odds with the tightly controlled digital yuan. Thankfully, the people of China will still be able to access Bitcoin through VPNs. Bitcoin will continue to be there for them should they ever need it — regardless of where Chinese miners relocate to.

Most importantly, this is a gigantic opportunity for Bitcoin to address two of its most frequently overblown criticisms: its reliance on Chinese miners, and the carbon footprint that this reliance entails. We have seen an overwhelming number of Environmental, Social, and Governance (ESG) initiatives pop up as direct responses to concerns around Bitcoin’s carbon footprint.

With this in mind, the timing of the CCP’s latest wave of regulatory scrutiny could not have been better. The ensuing miner exodus currently taking place is one of the most positive fundamental developments for Bitcoin in 2021. Even if we see short term drops in monthly implied hash rate figures as miners emigrate, it would be for an important cause.

A huge focus of our work at Coin Metrics these days is to monitor the health of various crypto networks. Beyond metrics like hash rate, we actively track network attacks, such as 51% attacks, across major PoW networks. If you are concerned about Bitcoin’s susceptibility to attacks in light of a potential short term drop, rest assured: you shouldn’t be. It is very unlikely that a decrease in monthly implied hash rate figures would meaningfully impact Bitcoin’s security.

Bitcoin currently overpays for its security by a wide margin if you consider the sheer amount of electricity and hardware resources that would be required to successfully attack it. Even if monthly implied hash rate were to drop in half and essentially go back to levels not seen since November 2019, the network would still be incredibly resilient against attacks.

The only meaningful impact a decrease in hash rate would entail would be longer block times. This happens when the mining difficulty parameter is too hard relative to the number of miners online, which leads to blocks being mined at a slower rate. While the network might become more congested as result, Bitcoin naturally readjusts difficulty roughly every two weeks so this would be a short-term phenomenon.

On the other hand, if we don’t see a considerable decrease in monthly implied hash rate, but miners still geographically disperse, Bitcoin will have become substantially more decentralized at the expense of short-term price volatility. A good trade if you ask me.

This is a guest post by Lucas Nuzzi. Opinions expressed are entirely their own and do not necessarily reflect those of BTC Inc. or Bitcoin Magazine.